News

All News

Video

Watch: Puerto Rico & Hawaii: Building Power with Energy Democracy

How can communities build power in the face of colonization, natural disasters, and corporate profiteering? In Puerto Rico and the Hawaiian island of Molokai, residents have been grappling with some of the highest energy costs in the nation, while for-profit …

Learn More

blog News

blog News

Read: A New Tool to Take on Predatory Landlords and Fight Evictions

News

News

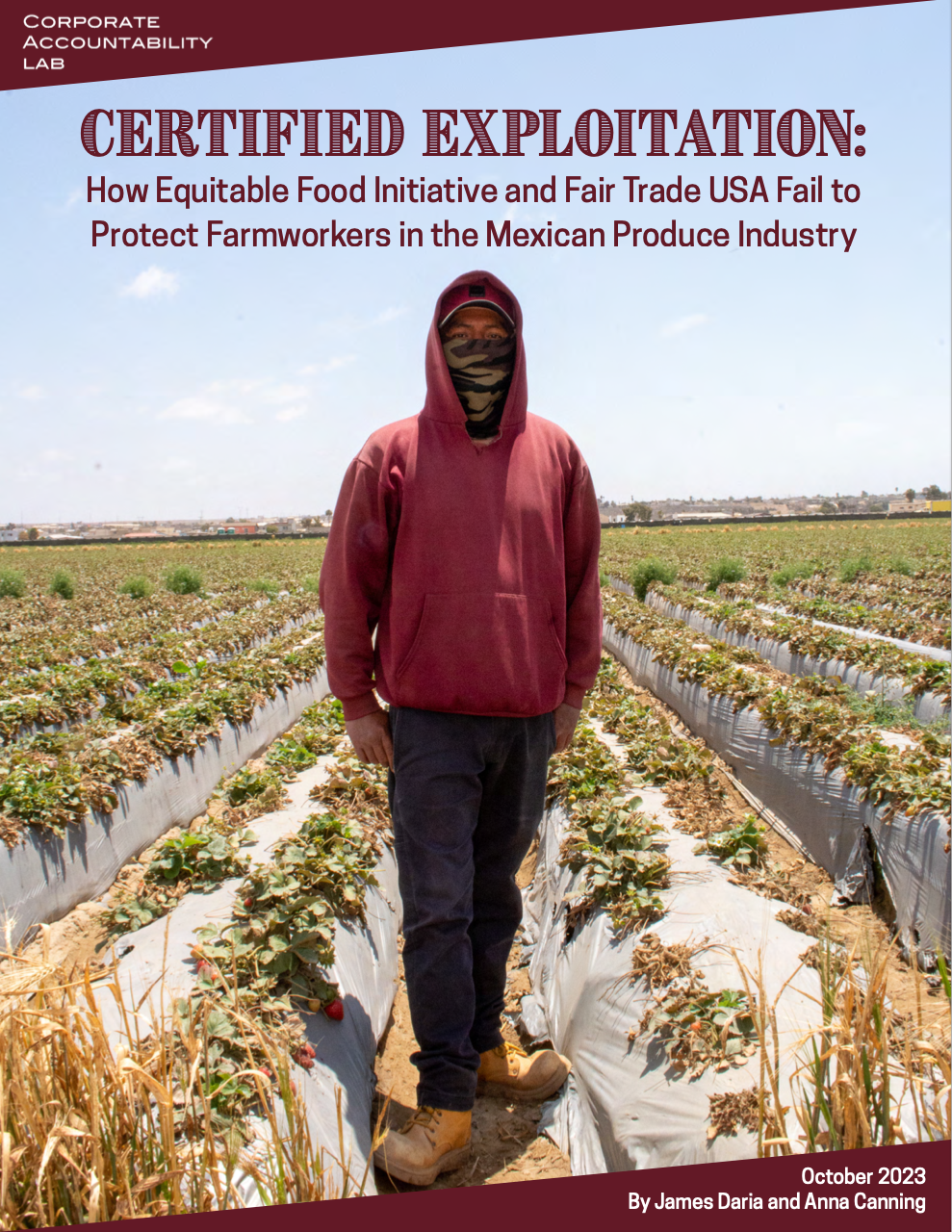

Why Fair Trade Produce Labels Are Bogus

blog News

blog News

Listen: A World Without Police: Featuring Geo Maher, Andrew Hairston, & Tafari Melisizwe

blog News

blog News

Pursuing Co-Governance in Chicago

blog News

blog News

Partners for Dignity & Rights Calls for an Immediate Ceasefire and an End to the Occupation

blog News

blog News

Majelia Ampadu has joined Partners for Dignity & Rights as our New Development Coordinator

Audio

Audio

Listen: Cooperatives Challenging Capitalism: Tamara Prosper and Tamah Yisrael of Cooperation New Orleans

Video

Video

Watch: Governing Power: Movement Strategies in the US and the Global South

blog News

blog News

Niki Franco has Joined Partners for Dignity & Rights as our Organizing and Partnerships Director

News

News

Hiring: Interim Communications Consultant for Dignity in Schools Campaign

News

News

Listen: Our Struggle is to Indigenize: Judith Le Blanc of Native Organizers Alliance on The Next World Podcast

Audio

Audio

Listen: Ending Corporal Punishment in Schools: With Janice Harper, Kameisha Smith, Katie Coates & Tafari Melisizwe

News

News

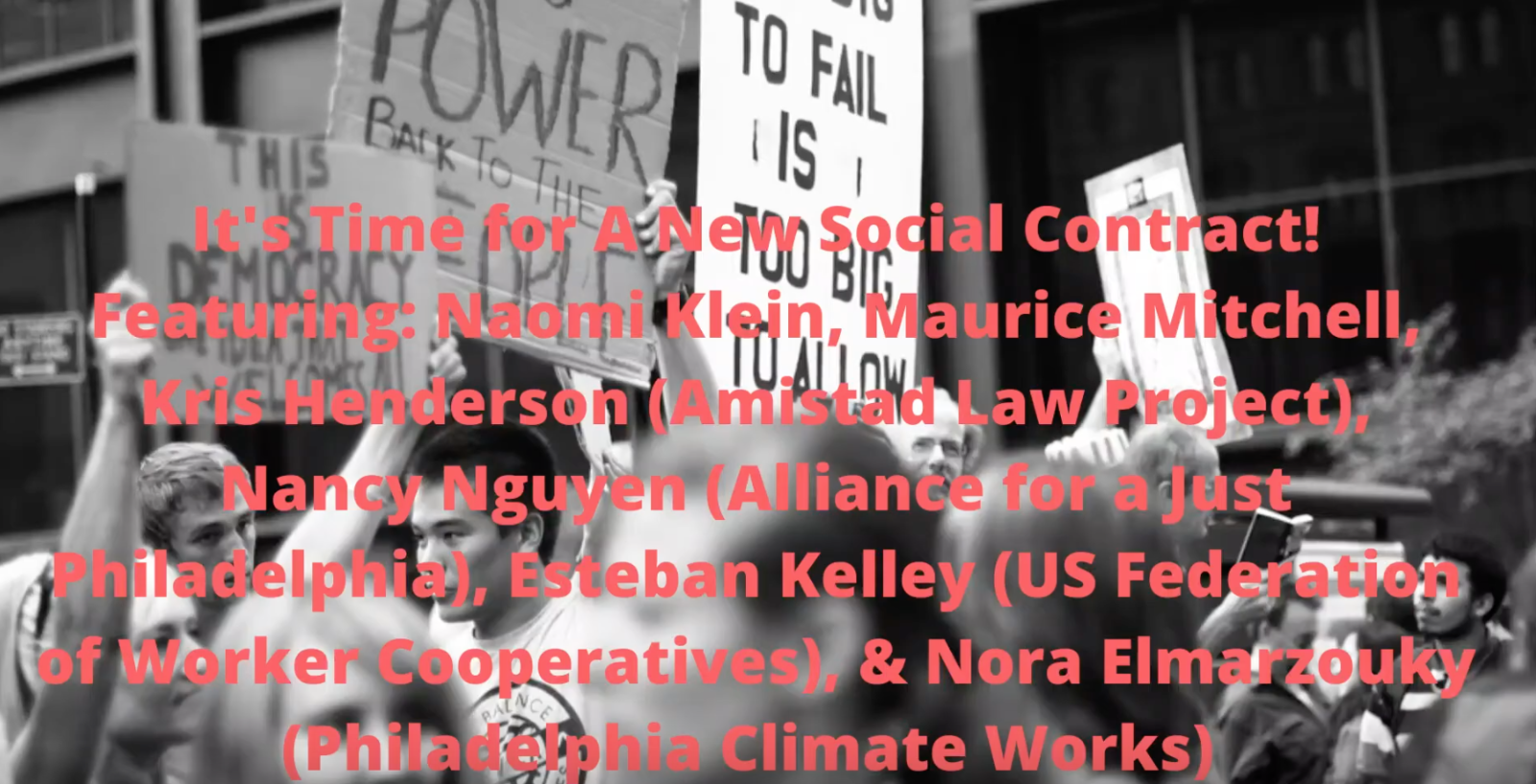

Sign the Petition to Support a New Social Contract

Audio

Audio

Listen: Co-Governing Toward Multiracial Democracy Podcast

blog

blog

Join Partners for Dignity & Rights at The 22nd Century Conference

News

News

Statement Against The Criminalization of Solidarity

News

News

Article: The Dirty Little Secret—Rising Property Values Are Incompatible with Affordability

News

News

Hiring: Development Coordinator, Partners for Dignity & Rights

News

News

Article: How to Build Multiracial Democracy at the Local Level

Audio

Audio

Listen: Rukia Lumumba from the People’s Advocacy Institute, Jackson, Mississippi

News

News

Article: Building Bottom-Up Democracy Through Co-Governance

News

Job Announcement: Organizing and Partnerships Director

News Video

News Video

Watch: “Co-Governing Toward Multiracial Democracy” Report Launch and Webinar

News

News

Sarah Newell of WSRN Discusses Corporate vs. Worker-driven Social Responsibility

News

Job Announcement: Dignity in Schools Campaign-New York Membership and Campaign Director

blog News

blog News

The Year in Worker-driven Social Responsibility

News

News

Dairy Workers Call on Hannafords for Justice

News

News

Worker-driven Social Responsibility Model Adopted by More Workers and Industries

News Video

News Video

Dignity in Schools Week of Action

Audio News

Audio News

Listen: Black Land and Black Liberation with Njera Keith and Kristina Brown of 400+1

News

News

Listen: Seventeen Years After Hurricane Katrina, Still Organizing for Education Justice

News

News

Listen: Art and Abolition With Bryonn Bain, Author of Rebel Speak: A Justice Movement Mixtape

News Video

News Video

Watch: From the Ground Up: Community Centered Policies to Scale Equitable Development – From our New Social Contract Webinar Series

Audio News

Audio News

Listen: Food Justice and Black Liberation on The Next World Podcast

News

News

Victory: Victoria’s Secret pays $8.3 million dollars in wage theft settlement

News

News

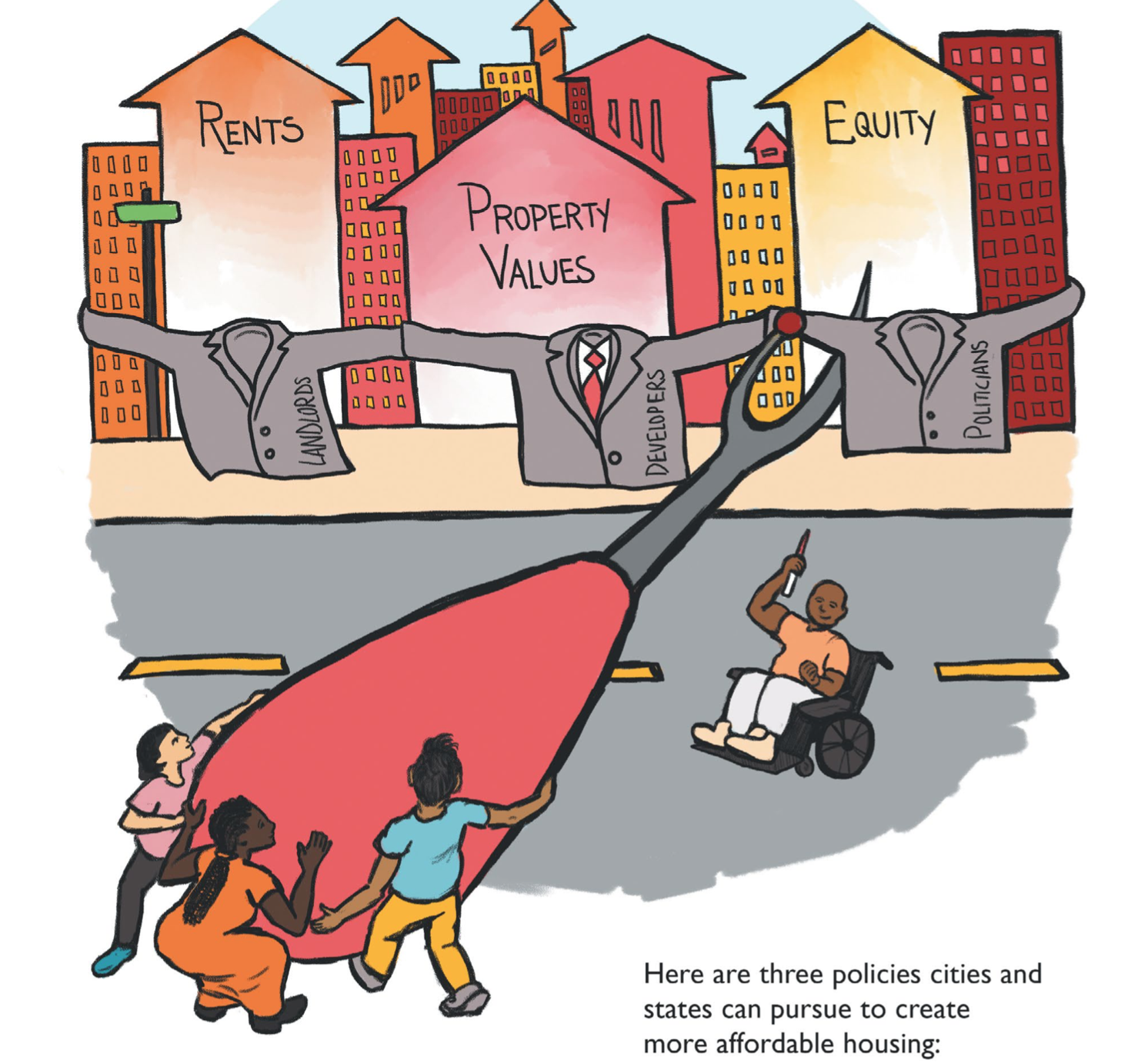

Advancing Housing Justice: Three Key Steps

blog News

blog News

Our Response to the Supreme Court Decision to Overturn Roe v Wade

News

News

Dignity in Schools Statement on the Killings in Uvalde, TX

News

News

Grief, Rage and Resistance: Our Statement on the Killings in Buffalo

Video

Video

Video: Rob Robinson on Panel on Poverty and Human Rights

News Video

News Video

New Social Contract Webinar Series: Cultivating Food Justice

News

News

A New Investment in Our Future

News

News

Solidarity with the Shackdwellers Movement in South Africa

News

News

On International Women’s Day 2022, We Join With Women on the Front Lines

News

News

The American Prospect on Put People First! PA’s Public Advocate Campaign

News

News

Remembering Paul Farmer

News

News

Our Work for Economic Democracy

News Video

News Video

New Social Contract Webinar Series: Privatization or Economic Democracy?

News

News

Jessica Chaves Tavares has joined Dignity in Schools Campaign as National Field Organizer

News

News

Announcing our New Co-Executive Director!

News Video

News Video

Watch: Partners for Dignity & Rights Co-Founders in Dignity in Schools Discussion

News

News

Dignity in Schools Campaign in New Book

News

News

Watch: Organizing for Victory: Fighting for Healthcare for All in New York

News

News

The Transformative Potential of Community Land Trusts

News Video

News Video

WATCH: Affordable for Whom?: An Online Summit on Community Controlled, Deeply Affordable Housing

News Video

News Video

Watch: How do we invest in our communities?

News

News

Democratizing Workers’ Compensation: Our Final Workers’ Comp Hub Newsletter

News

News

Labor and Community Organizations Call on Health Care Task Force to Prioritize Human Rights

News

News

We Must Fight Privatization of Medicare and Medicaid to Win Universal Health Care

News

News

New Video: The Billionaires Exploiting Garment Workers

News

News

Affordable for Whom?: An Online Summit on Community Controlled, Deeply Affordable Housing

News

News

Letter to Congress: It’s time to Expand and Improve Medicare

News

News

Job Announcement: Co-Executive Director

News

News

Latest on Partners for Dignity & Rights in the Media

News

News

New Video: Pay Women Garment Workers a Living Wage!

News

News

Partners for Dignity & Rights Announces Co-Executive Director Leadership Transition

News

News

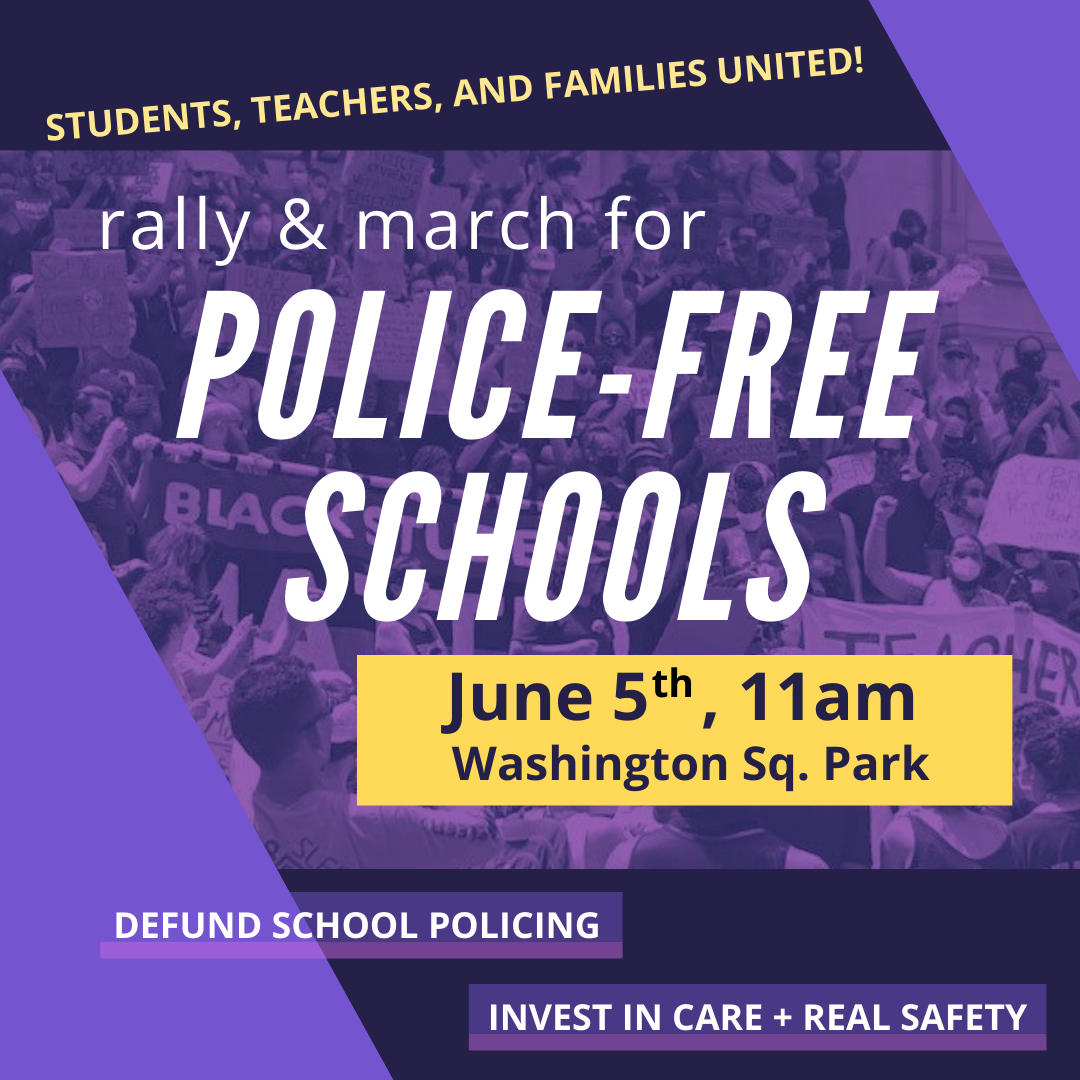

June 5 Rally & March for Police-Free Schools

News

News

Partners for Dignity & Rights Joins 48 Organizations in Call on Biden to Include Bold Drug Pricing Reforms in the American Families Plan, Use the Savings to Expand Medicare

News

News

Listen: Ben Palmquist, Program Director, Health Care and Economic Democracy, on Citations Needed Podcast

News

News

Is Conviction Justice?

News

News

Listen: Liberating Housing on The Next World Podcast

News

News

Rising Against Anti-Asian Discrimination and Violence

News

News

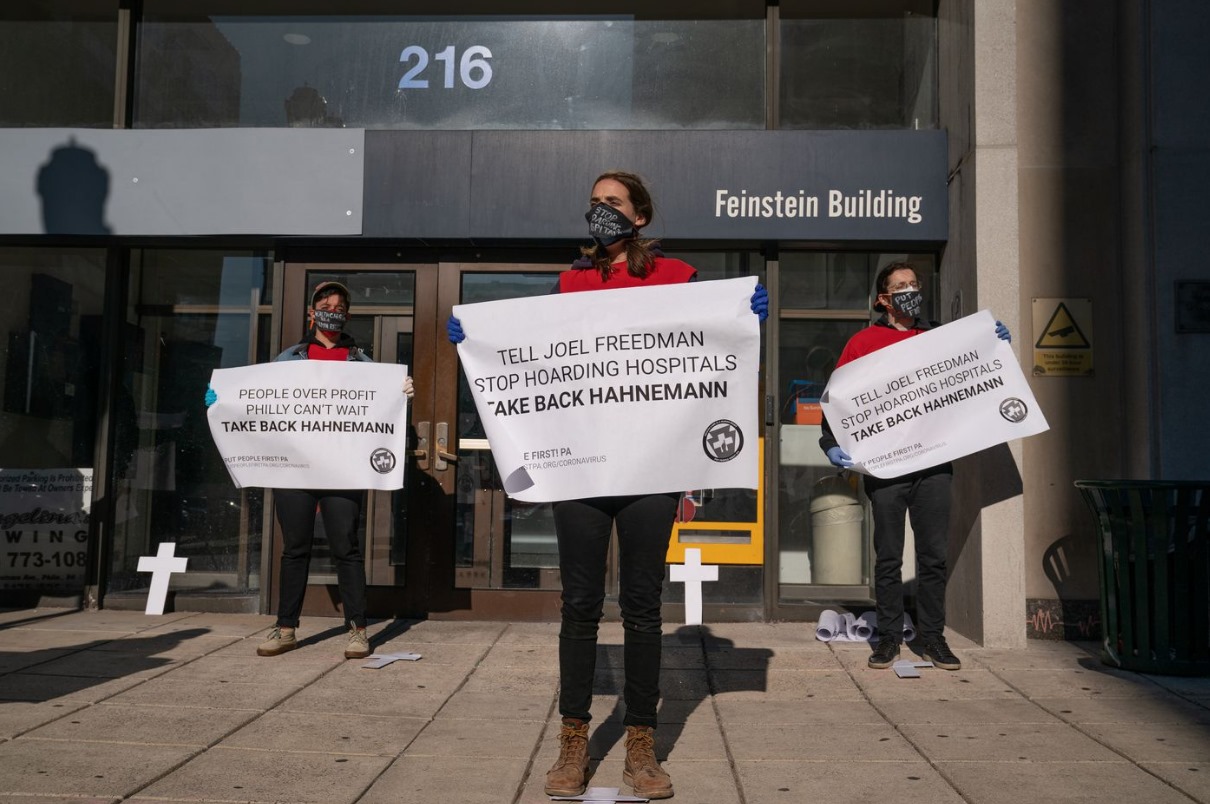

Don’t Let Hospital CEO’s Shut Down Care

News

News

How the U.S. Health Care System is and isn’t Working

News

News

Beyond Survival One Year Later

News

News

New Video: Respect Garment Workers!

News

News

Democratizing Governance to Advance Health Justice and Economic Democracy

Audio News

Audio News

Interview on Medicare for All and health justice narratives on Oregon community radio

News

News

The Struggle for Healthcare Justice: It’s Movement Time

News Video

News Video

How to Change the Media Discourse to Win Medicare for All and a Multiracial Democracy

News

News

Health, Racial Disparities, and Economic Justice

blog

blog

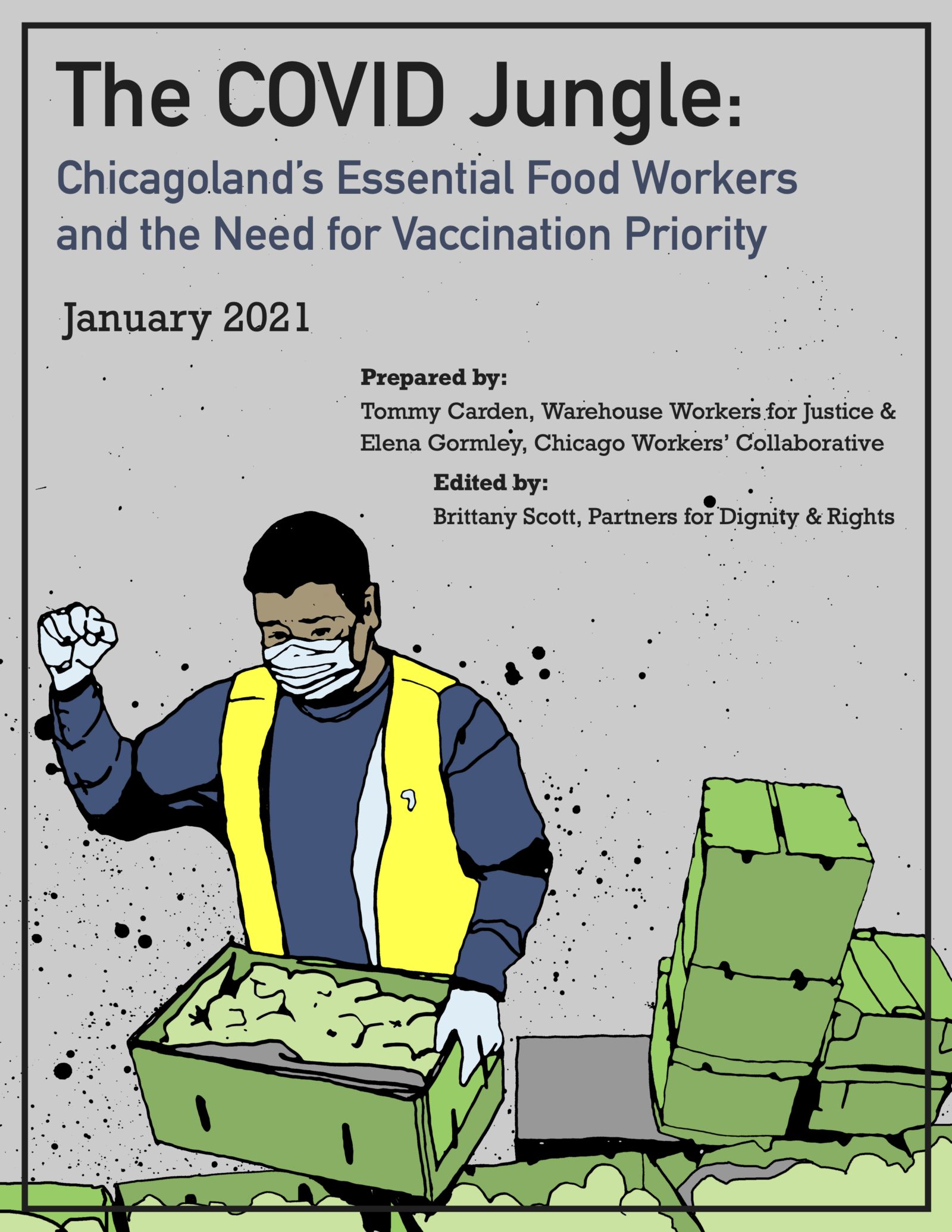

The COVID Jungle: Chicagoland’s Essential Food Workers and the Need for Vaccination Priority

News

News

New Episode of The Next World Podcast: M. Adams of Freedom Inc

News

News

Honoring Our Power – 15 Years of Dignity and Rights

News

News

Believe in NYC Schools: Safety Without Policing

News

News

New Episode of The Next World Podcast: Sterling Johnson and Jenn Bennetch of Philadelphia Housing Action

News Video

News Video

Whatever Happens, We are Ready to Keep Fighting

News Video

News Video

Watch: It’s Time for a New Social Contract

News

News

The Stakes Could Not Be Higher

News

Hiring: Director of Development, Partners for Dignity & Rights

News

News

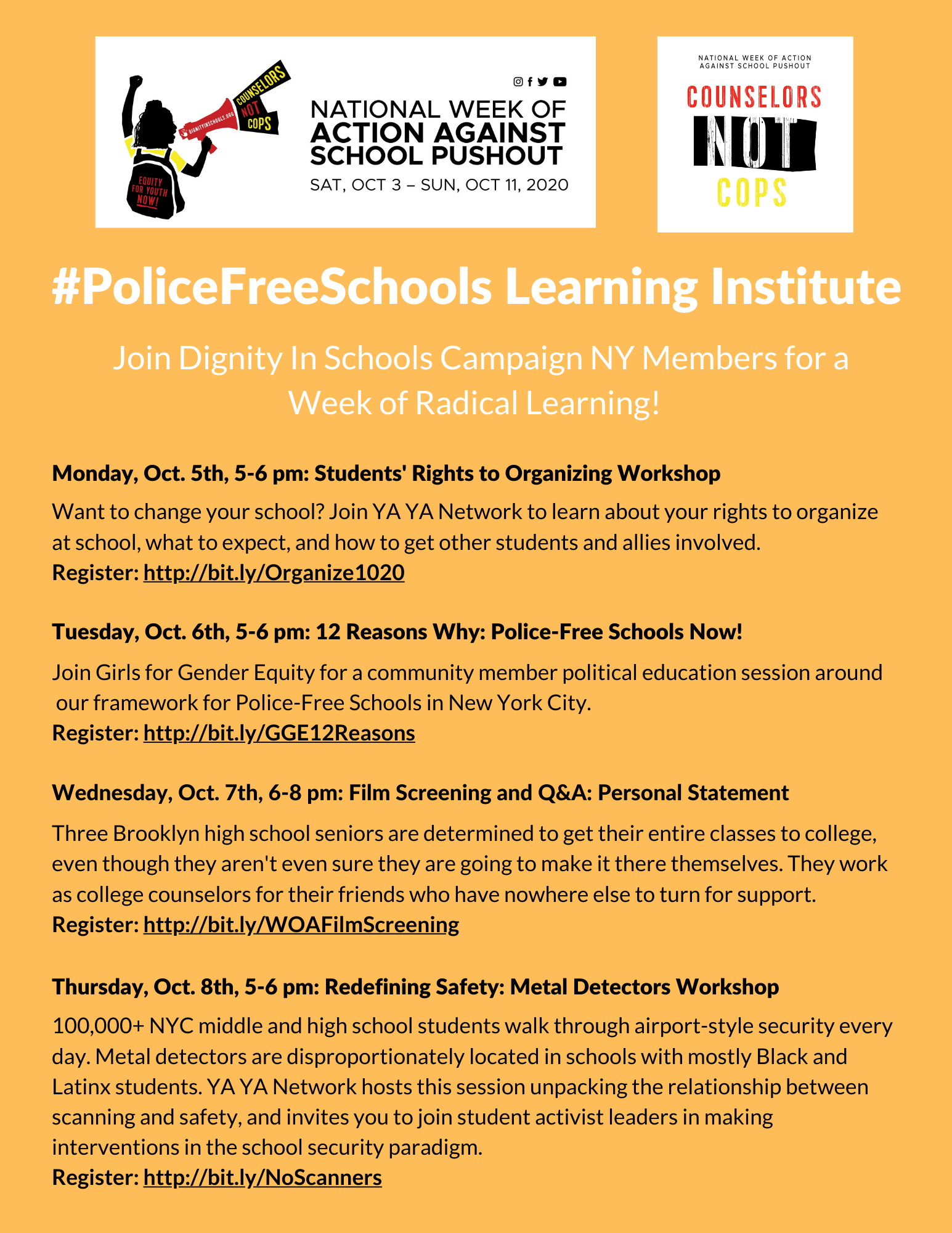

#PoliceFreeSchools Learning Institute Schedule: Join Dignity in Schools Campaign-NY Members for a Week of Radical Learning

News

News

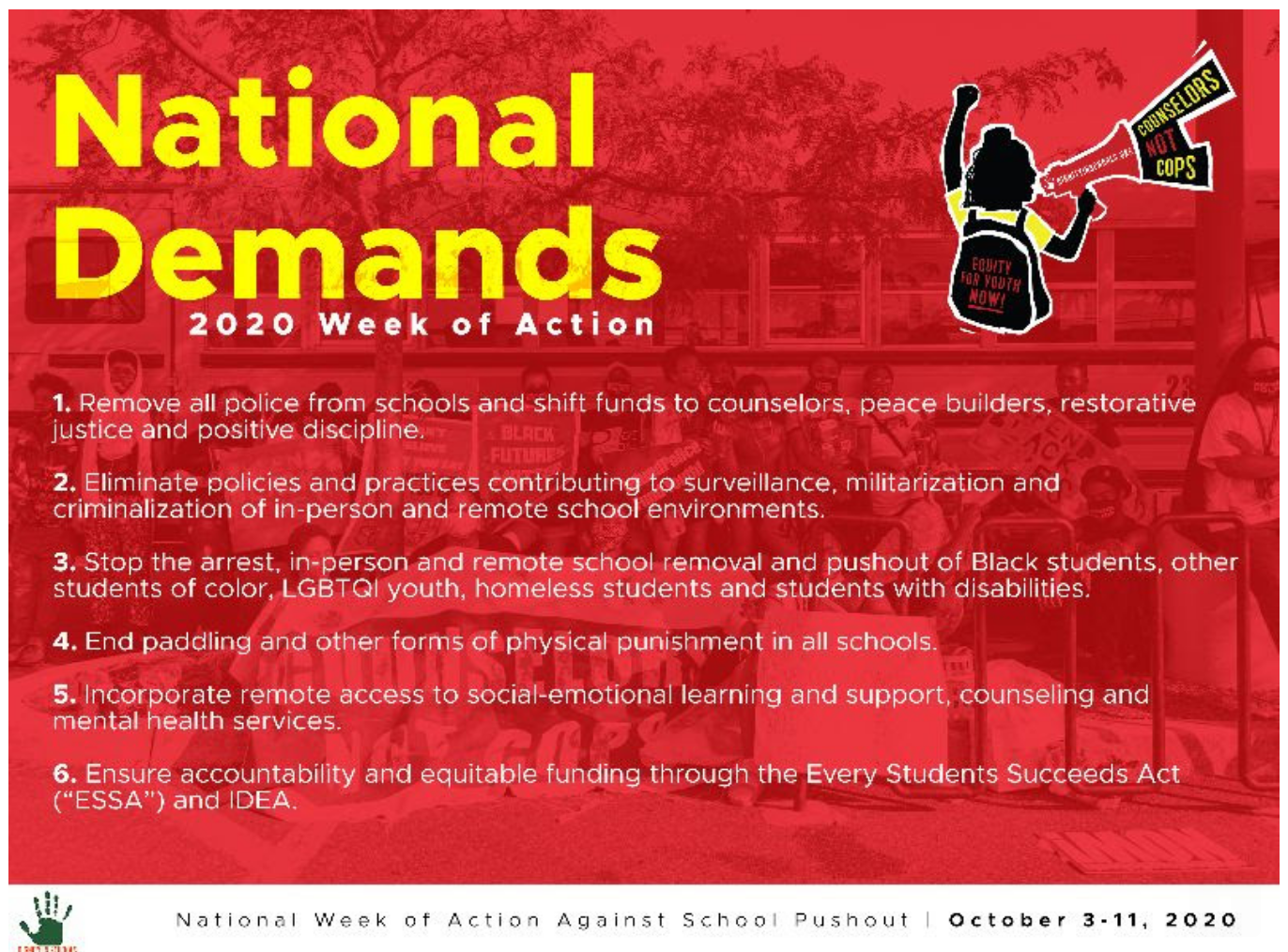

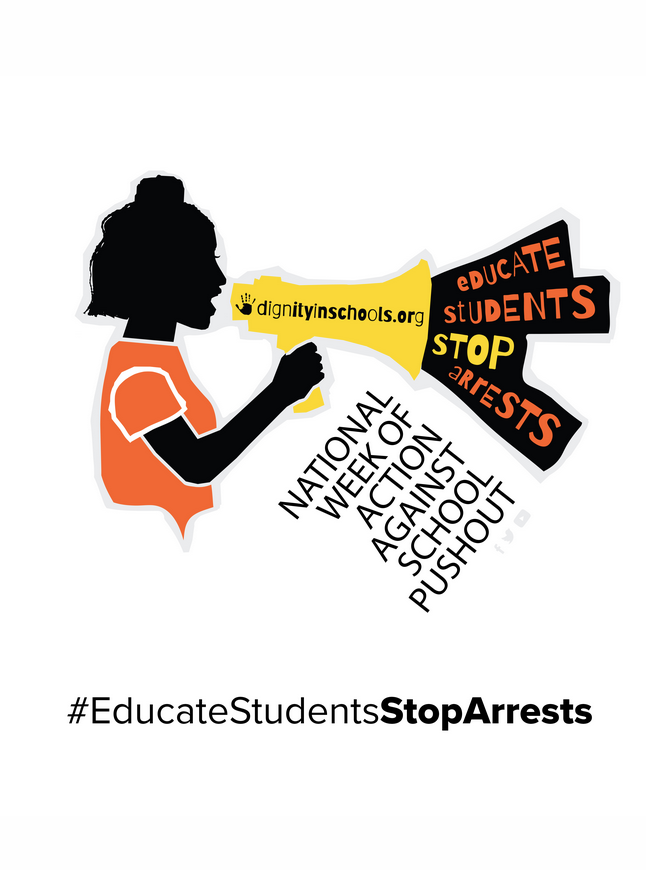

Join the National Week of Action Against School Pushout: October 3 – 11, 2020

News

News

Request For Qualifications: Research Consultant on Deeply Affordable Housing Development

News

Paid Internship with Partners for Dignity & Rights: Fair Development Research

News

News

The Power of Labor

News

News

We are Excited to Announce our new Co-Executive Director!

News

News

UN expert urges a ban on evictions during COVID-19 pandemic

News

News

Housing Now! Listen to the Latest Episode of The Next World Podcast

News

News

Join us in Saying No to Austerity and Police Budgets, Yes to Democracy and Human Needs

News Video

News Video

Watch: Honoring Our Power: Community Solutions in a Time of Crisis

News

News

How to Make This Year’s Eviction Crisis Our Last

News

News

Can We Learn from COVID-19?

News

News

Solidarity Statement from Abahlali baseMjondolo (South African Shack Dwellers Movement) to Black Lives Matter

News

News

Defund Police, Invest in Transformative Justice

News

News

To Fight COVID–19, We Need to Build Worker Power and Worker Safety

News

News

Addressing Our Real Deficits: Democracy and Human Rights

blog

blog

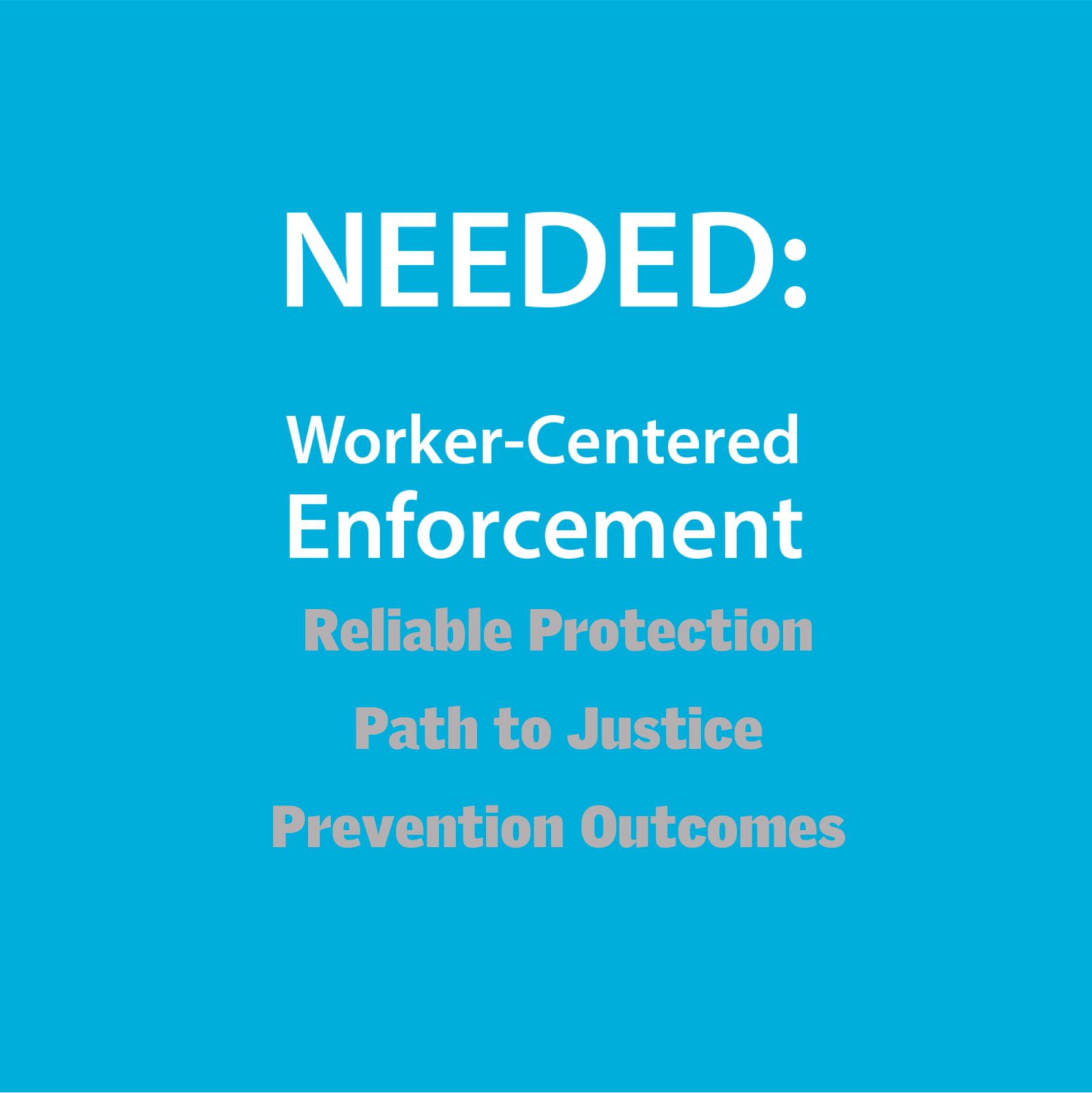

Building Worker Power into Standard Setting, Monitoring and Enforcement

News Video

News Video

Watch: Naomi Klein, Maurice Mitchell, and Cathy Albisa on a New Social Contract

blog

blog

No Turning Back: How the Pandemic Opens the Door to a New Economy for People and the Planet

blog News

blog News

The U.S. Has Eliminated Thousands of Hospital Beds in the Last Ten Years, Exacerbating the Current COVID-19 Crisis

blog

blog

From Free CovidCare to Medicare For All

News

News

A Goodbye from Cathy Albisa, Co-Founder and Executive Director of Partners for Dignity & Rights

News

News

Reports from the Frontlines of COVID-19

News

News

Calls to Action in Response to COVID-19

News Video

News Video

Watch: New Hampshire People’s Issues Forum Supports A New Social Contract for Workers

News

News

Our Statement on COVID-19/Coronavirus and Human Rights

News

News

Single-Payer Health Care Did Not Fail in Vermont

News

News

[Closed] Part-Time Health Care Justice Research Assistant

News Video

News Video

Watch: Senator Bernie Sanders endorses A New Social Contract for Workers

Audio News Video

Audio News Video

Listen: Do We Need a New Social Contract?

News

News

New Social Contract Tour Coming to a City Near You

News

National Economic and Social Rights Initiative is now Partners for Dignity & Rights

News

News

Black Lives Matter at School Week, Feb. 3-7, 2020

News

News

Watch this new video from the Worker-driven Social Responsibility Network

News

News

Vermont Workers’ Center Medicaid Assembly at the State House

News

News

Jobs for All: A Manifesto

News

News

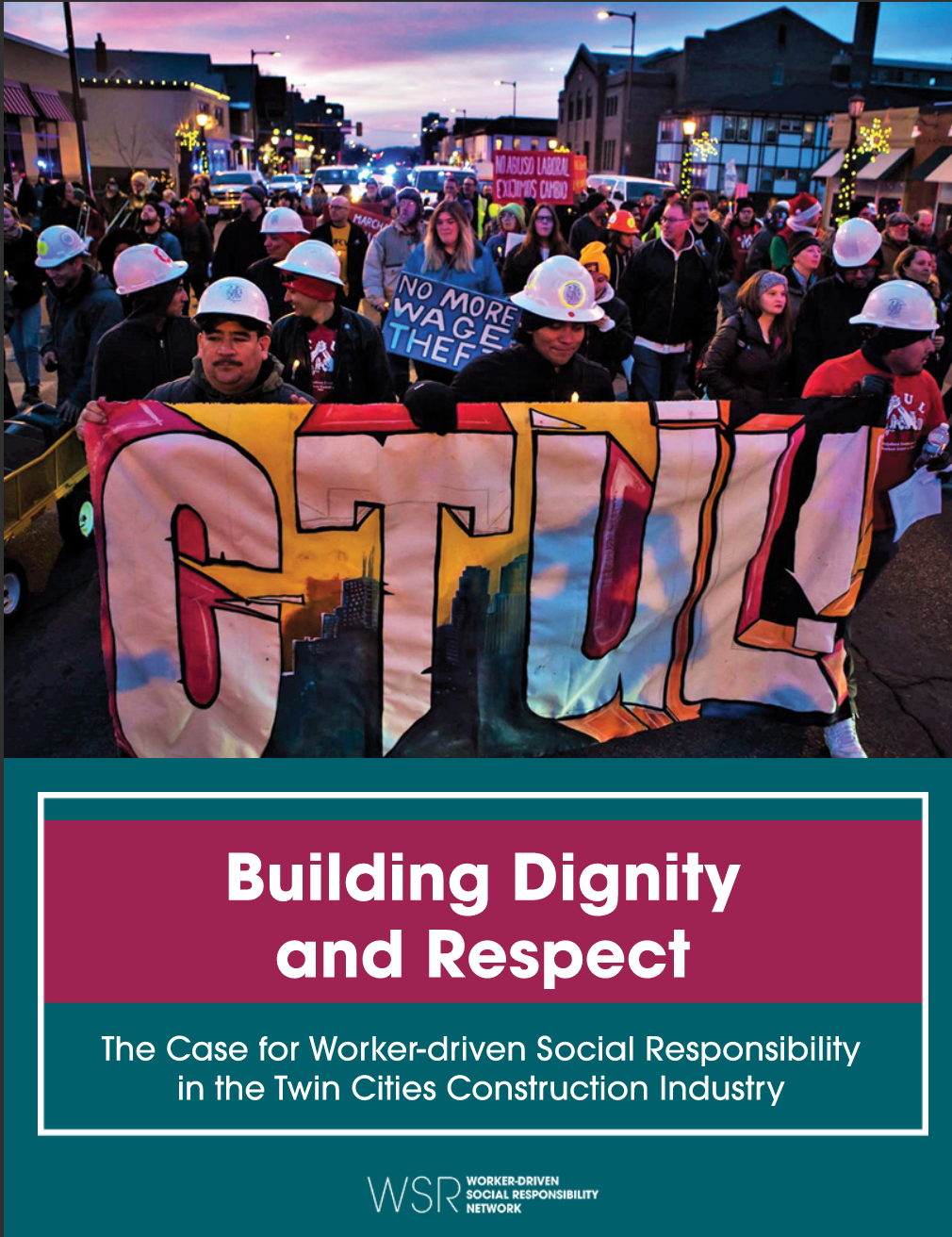

Building Dignity and Respect

News

News

Commemorating Human Rights Day

blog

Save The Date for our 15th Anniversary Celebration

blog

blog

Commemorating Indigenous Resistance

News

News

Senator Bernie Sanders Endorses New Social Contract for Workers

News Video

News Video

Watch: Philly Organizers on Building a New Social Contract

News

News

Building Worker Power: Moving Beyond Standards to Enforcement

News

News

Join Dignity in Schools Campaign for 10th National Week of Action Against School Pushout

News

News

Why the Argument that Medicare for All Will Curtail “Freedom” Is So, So Wrong

News

News

Take Action! Make Big Polluters Pay to Address the Climate Crisis They’ve Caused

News

News

The Future Belongs to Globalists

News

News

A New Social Contract for Workers – See Report

News

News

Expect More Health Industry Spin At Thursday’s Democratic Debate

News

News

Partners for Dignity & Rights Director Cathy Albisa to Receive Human Rights Award

News

News

New Social Contract Tour

News

News

National Affordable for Whom Conference – 2019

blog

blog

Workers’ Comp Hub Newsletter: Summer 2019

News

News

Economists endorsed a unified public insurance system, not a fractured multi-payer insurance system

News

News

Fairness and Accuracy in Reporting on how the health insurance industry warped media coverage

News

News

REPORT: Media Repeating Insurance Industry Talking Points

News

News

More than 250 economists sign letter backing Medicare for All

News

News

Responding to Rising Tide of anti-Semitism and Islamophobia

News

News

Leader of Brazil Landless Workers’ Movement Visits NYC

News

News

Our Statement on Recent Arsons in the U.S. South

News

News

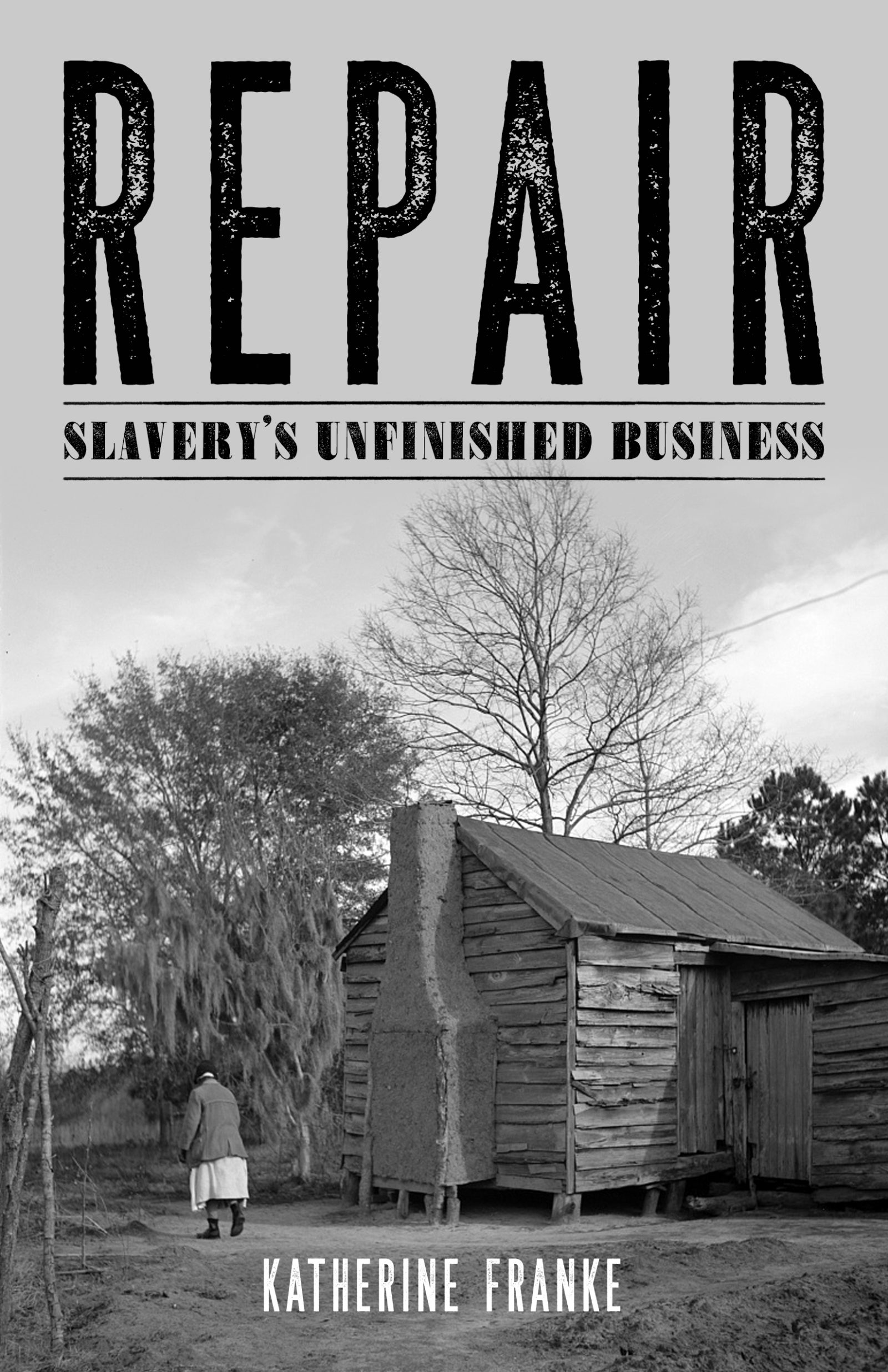

Save The Date for Grounding Reparations: Community Land Ownership & Racial Equity

News

News

The Nation on “The Human-Rights Agenda Underlying the 2019 Medicare for All Bill”

News

News

Our statement on attacks on Muslims in New Zealand

News

News

Our Statement on International Women’s Day

News

News

New Release: Human Rights Assessment of Medicare for All Act of 2019

News

News

Common Dreams: Jayapal’s Medicare for All Bill ‘Sets a New Standard’ for Guaranteeing Healthcare as a Human Right

News

News

What is the national health care debate really about? Splinter breaks it down.

News

News

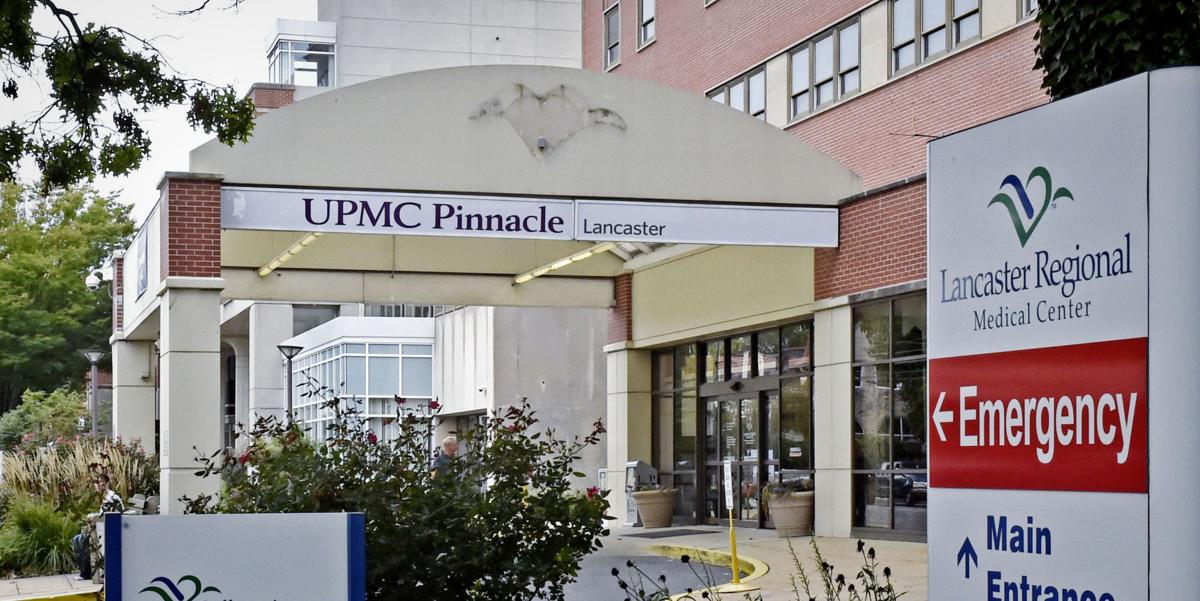

Protest expected Wednesday afternoon outside county government building against UPMC Pinnacle closure

blog

Workers’ Comp Hub Newsletter: Winter 2019

blog News

blog News

Workers’ comp news from around the country

blog News

blog News

Punitive Policies Target Low-Wage Workers, Create Barriers to Workers’ Comp

News

News

The next six months in the politics of universal health care

News

News

Put People First! Pennsylvania Members Fight to Keep Hospital Open

News

News

Medicaid work requirements don’t work. Maine was right to reject them.

News

News

On MLK Day: Add Your Name Supporting A New Social Contract

News

News

Mainers organize to defend Medicaid

News

News

Press Release: Students of Color and Community Organizations From Across the Country Respond to Federal Commission on School Safety Findings

News

News

We Support Love Knows No Borders: A Moral Call for Migrant Justice

News

News

Courage and Commitment on Human Rights Day

News

News

Partners for Dignity & Rights Joins With People’s Demands for Climate Justice

News

News

What do the midterm election results mean for health care?

News

News

Our Statement on the Killings at the Tree of Life * Or L’Simcha Congregation

News

News

Our Statement on the Killing of Maurice Stallard and Vickie Lee Jones in Jeffersontown, Kentucky

News

News

Report on UN Special Rapporteur on the Right to Housing Visit to New York City

News

News

We Stand in Solidarity with Transgender and Gender Nonconforming Communities

News

News

Maine Rally for Universal Health Care and Against Attacks on Medicaid

News

News

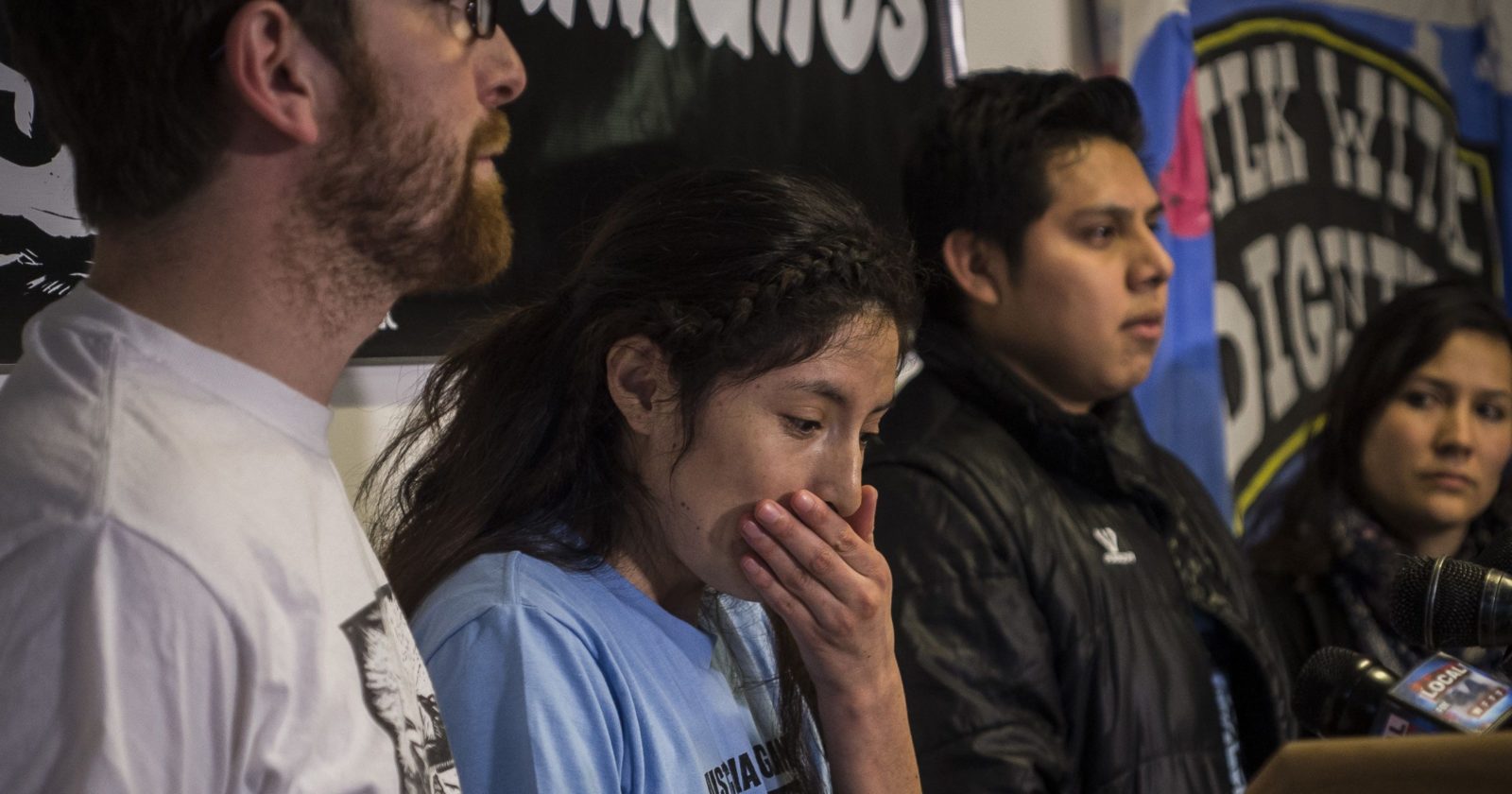

Labor Trafficking Case Exposes Endemic Abuse in Minnesota’s Construction Industry

News

News

Thousands Across the U.S. Join the March for Black Women

News

News

Complaint Filed Against Auditing Company for Ignoring Fatal Flaws in Garment Factory

News

News

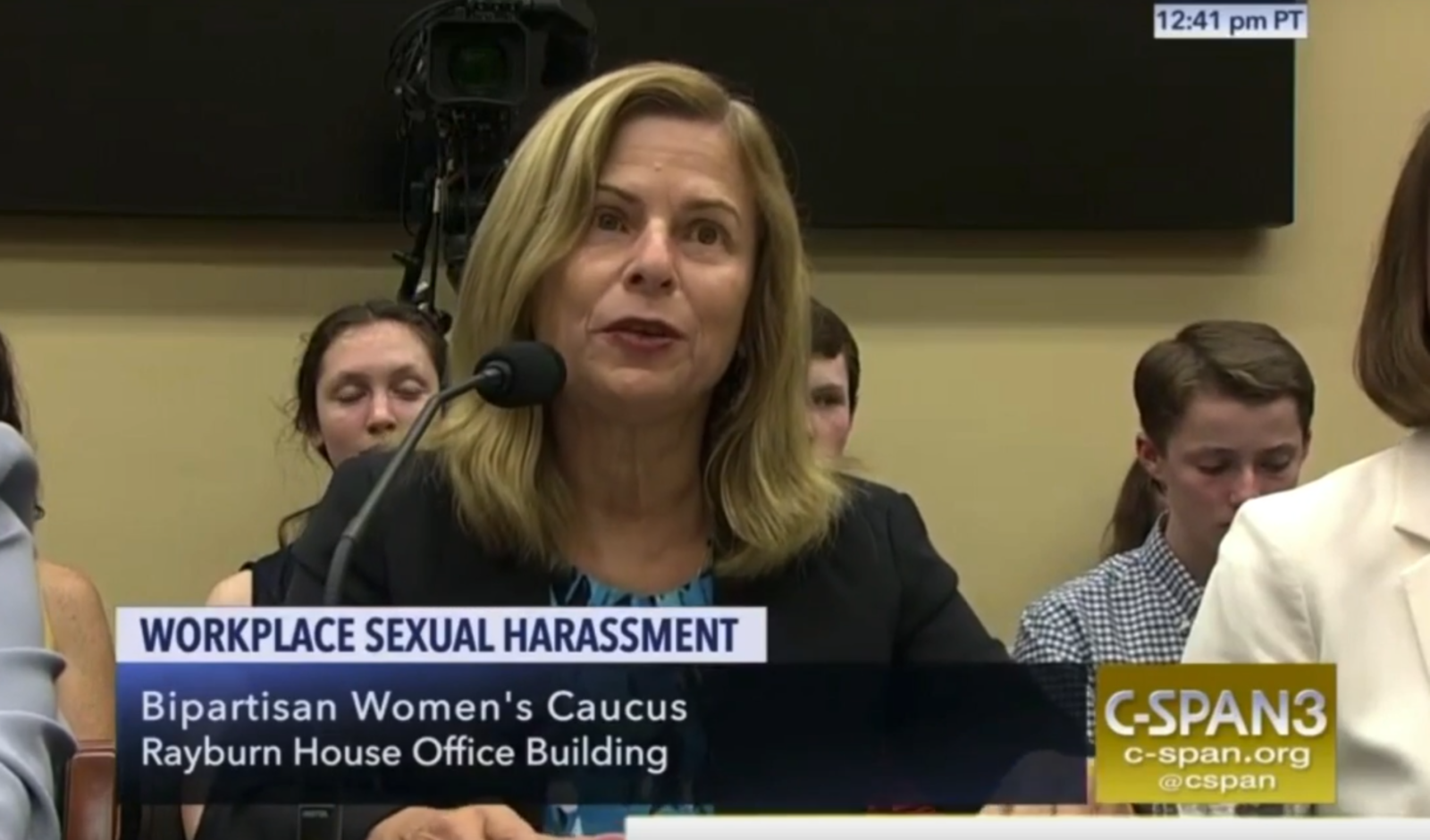

Congressional Women’s Caucus Hearing on Workplace Sexual Harassment Spotlights Fair Food Program

News

News

PUT PEOPLE FIRST! PA STATEWIDE WEEK OF ACTION

News

News

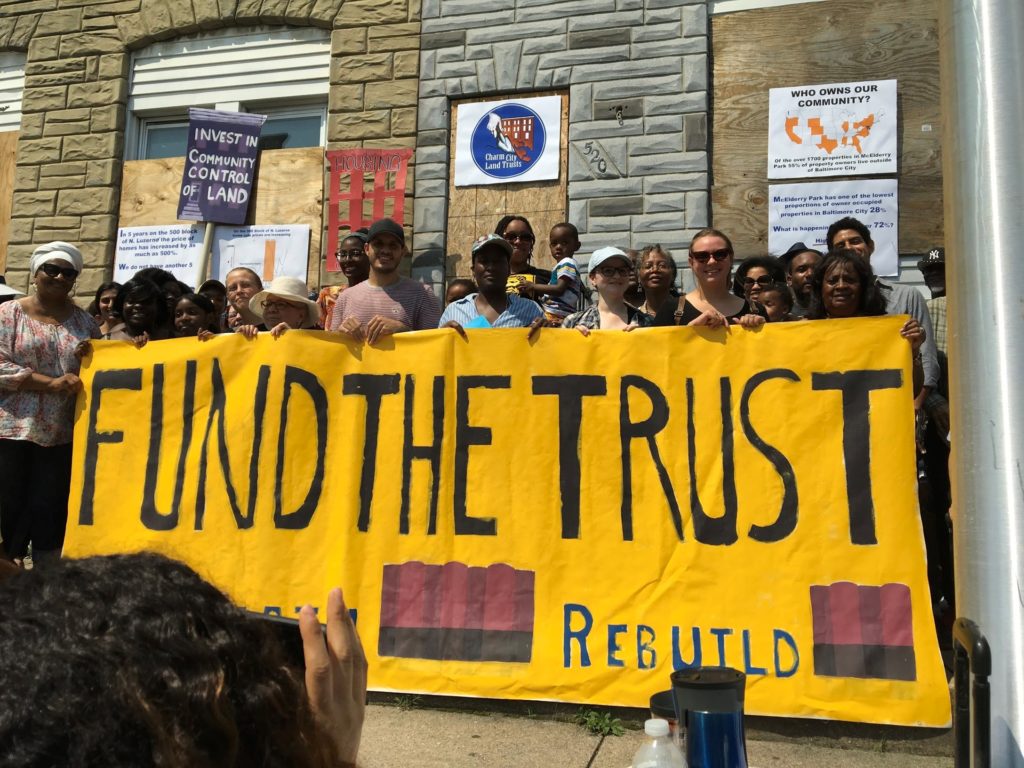

Victory in Baltimore: 20 Million Dollars for Permanently Affordable Housing

blog

blog

Workers’ Comp Hub Newsletter: Summer 2018

News

News

Healthcare is a Human Right Collaborative arrives in Hazleton

News Video

News Video

Watch: The New Social Contract: A Framework for Change

News

News

Open Democracy Article Highlights Advantages of Worker-Driven Social Responsibility

News

News

Dismissing Water as a Human Right is a Dangerous Path

News

News

Partners for Dignity & Rights at the Single Payer Strategy Conference

News

News

Medicaid Organizing Updates

News

News

Supporting a New Poor People’s Campaign

News

News

We Stand with Families Targeted for Abuse

News

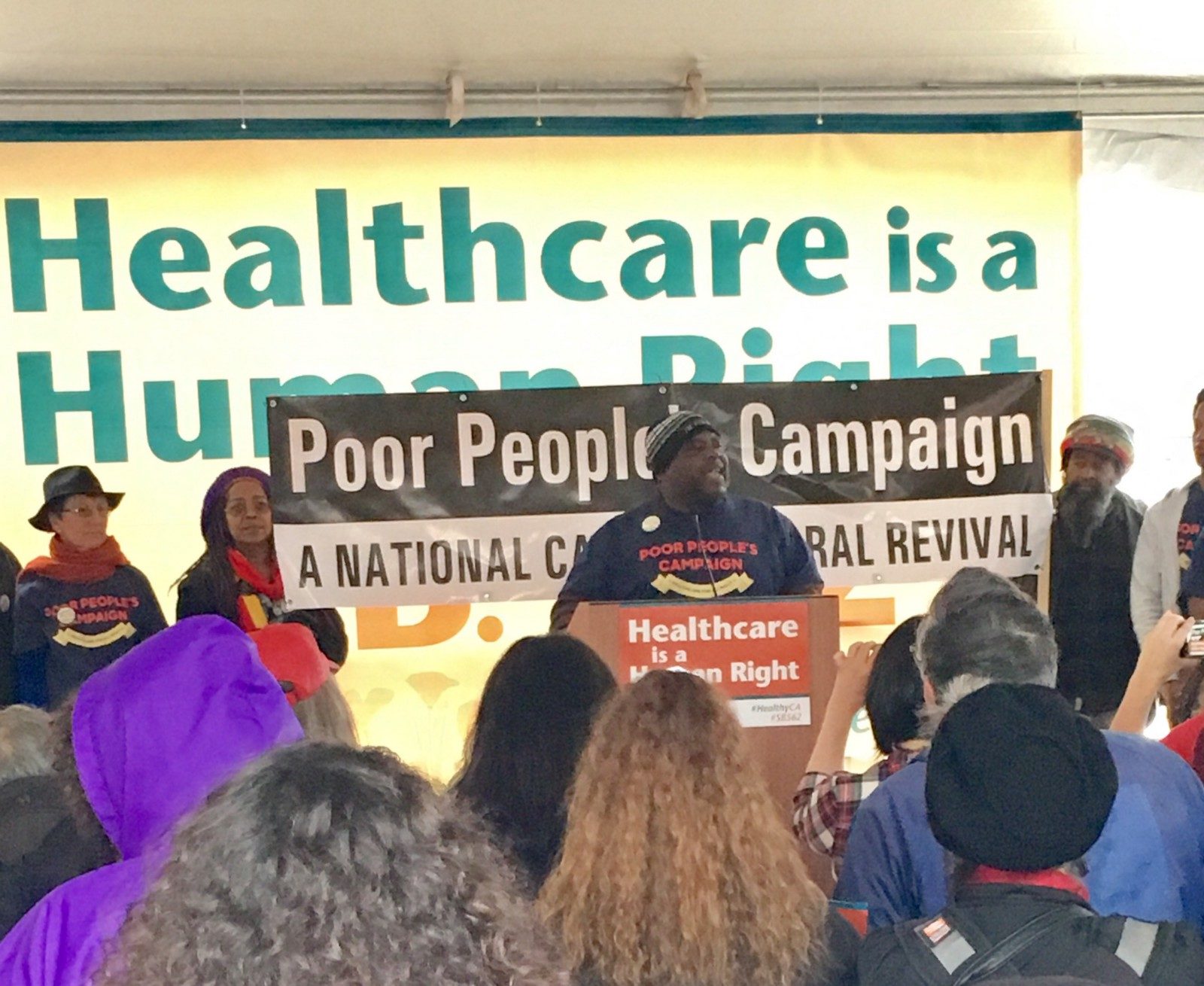

Building a Poor People’s Movement for Our Right to Healthcare

News

News

Wendy’s Can Run But Not Hide From its Responsibility to Workers

News

News

Photos and Video From the launch of A New Social Contract: Collective Solutions Built by and for Communities!

News

News

U.S. leads in income inequality and moving ‘full steam ahead to make itself more unequal’

News

News

Responsible Job Creation Act, New Temp Work Law, Goes Into Effect

News Video

News Video

Watch: A New Social Contract: Launch Event

News

News

A New Social Contract: Collective Solutions Built by and for Communities

News

News

Introduction Of City Charter Ballot Petition That Will Mandate Citizen Participation In Budget Making

News

News

Introduction of Speculation Tax with entire City Council sponsorship

News Video

News Video

Watch: Mia Charlene White, Imara Jones, and Cathy Albisa on a New Social Contract

News

News

Launching A New Social Contract Promoting Bold and Transformative Community-Driven Solutions to Inequity

blog

blog

Workers’ Comp Hub Newsletter: Spring 2018

News

News

Campaign Led by ARISE Chicago Leads to Bill Creating New Office of Labor Standards Enforcement

News

News

Debunking False Health Care Solutions on The Laura Flanders Show

News

News

State Bill Championed by Chicago Worker Centers Would Create New Enforcement Tool for Workers

News

News

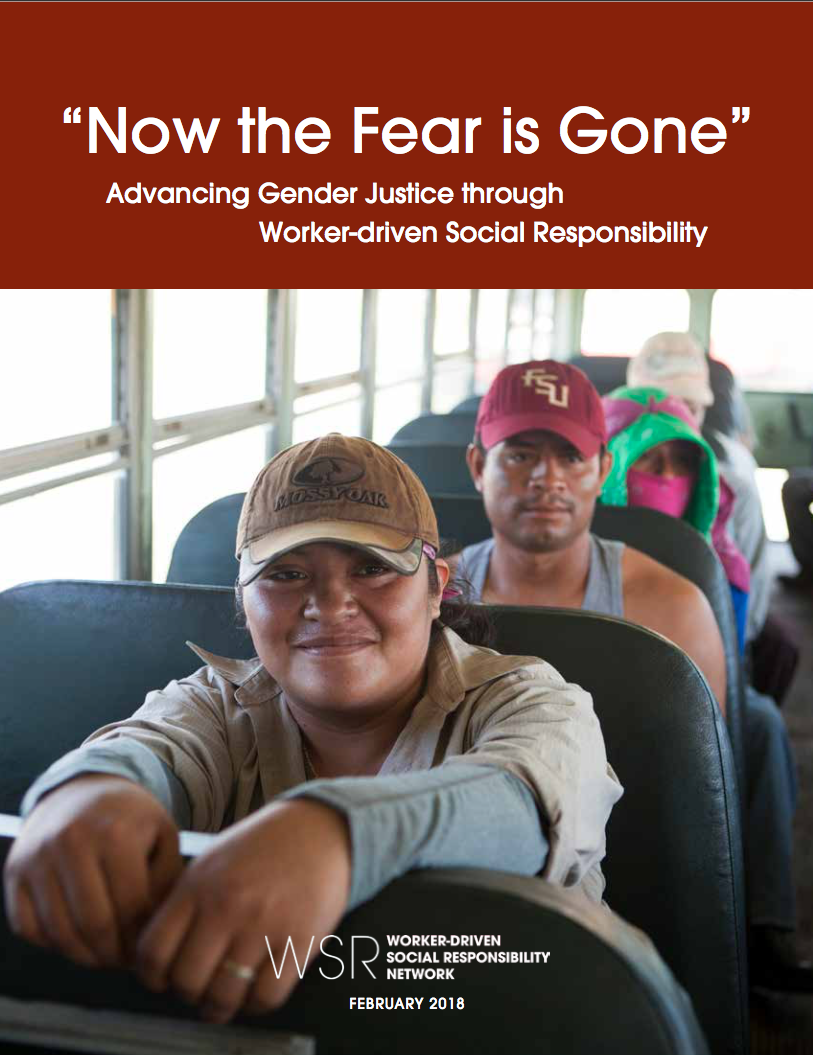

New Report: Advancing Gender Justice Through Worker-driven Social Responsibility

News

News

Partners for Dignity & Rights joins Healthy California for a legislative hearing, rally, and lobby day at the State Capitol

News

News

“How Power is Built from the Bottom”: CTUL, Minneapolis’ Worker Center Movement

News

News

Racial & Economic Equity, Not Market, Should Be North Star of Local Budget Policy

blog

blog

Workers’ Comp Hub Newsletter: Fall 2017

News

News

The Growing Movement for Worker-Driven Social Responsibility

News

News

New York Times: Ben & Jerry’s Strikes Deal to Improve Migrant Dairy Workers’ Conditions

News

News

The grassroots activists who paved the way for single-payer health care’s political moment

News

News

Single Payer Is on the National Agenda—And It’s Thanks to People’s Movements

News

News

Transformative Solutions to Guarantee Workers’ Rights

News

News

Reflecting on Charlottesville

News

News

Leveraging “Resiliency”

blog

blog

Workers’ Comp Hub Newsletter: Summer 2017

News

News

Data Shows Texas Employers Shift Costs of Workplace Injuries Onto Workers, the Public

News

News

Wake Forest Law Review: Preventing Forced Labor in Corporate Supply Chains: The Fair Food Program and Worker Driven Social Responsibility

News

News

Read in Truthout: Poverty Wages, Deportations, Wage Theft, Cockroaches: Farmworkers Demand Dignity from Ben & Jerry’s

News

News

Health Is a Right — Not a Commodity

News

News

Whose Dissent is Putting Them in Danger?

News

News

The Senate Health Care Bill Is an Assault on Human Rights

News

News

Wealthy Speculators Drive Up Home Prices in L.A. A New Tax on Them Could Make Housing Affordable

News

News

Shutting Out the Public from the Senate Healthcare Bill Isn’t Just Antidemocratic: It’s Deadly

News

News

From Coast to Coast: California shows that the road to universal, publicly funded health care runs through the states.

News

News

Prominent Human Rights Organizations Send Ben & Jerry’s Letter in Support of Milk with Dignity

News

News

Enrique Balcazar: “Why I am Marching to Ben & Jerry’s Ice Cream Plant”

News

News

VIDEO: How A $40 Million Affordable Housing Fund Could Transform Baltimore

News

News

In These Times: Trumpcare 2.0 Is a Death Bill. It’s Time to Fight for the System We Want

News

News

Workplaces in Chicago Have ‘Become Dangerous and Abusive Sweatshops’: Study

News

News

New Study Finds “More Sweatshops than Starbucks” in Chicago

blog

blog

Workers’ Comp Hub Newsletter: Winter/Spring 2017

News

News

Study Focuses On Retaliation Against Low-Wage Workers

News

News

Workers Face Retaliation for Speaking Out: Report

News

News

IL Survey of 300 Low-Wage Workers: Some Face Denial of Workers’ Comp Benefits, Retaliation

News

News

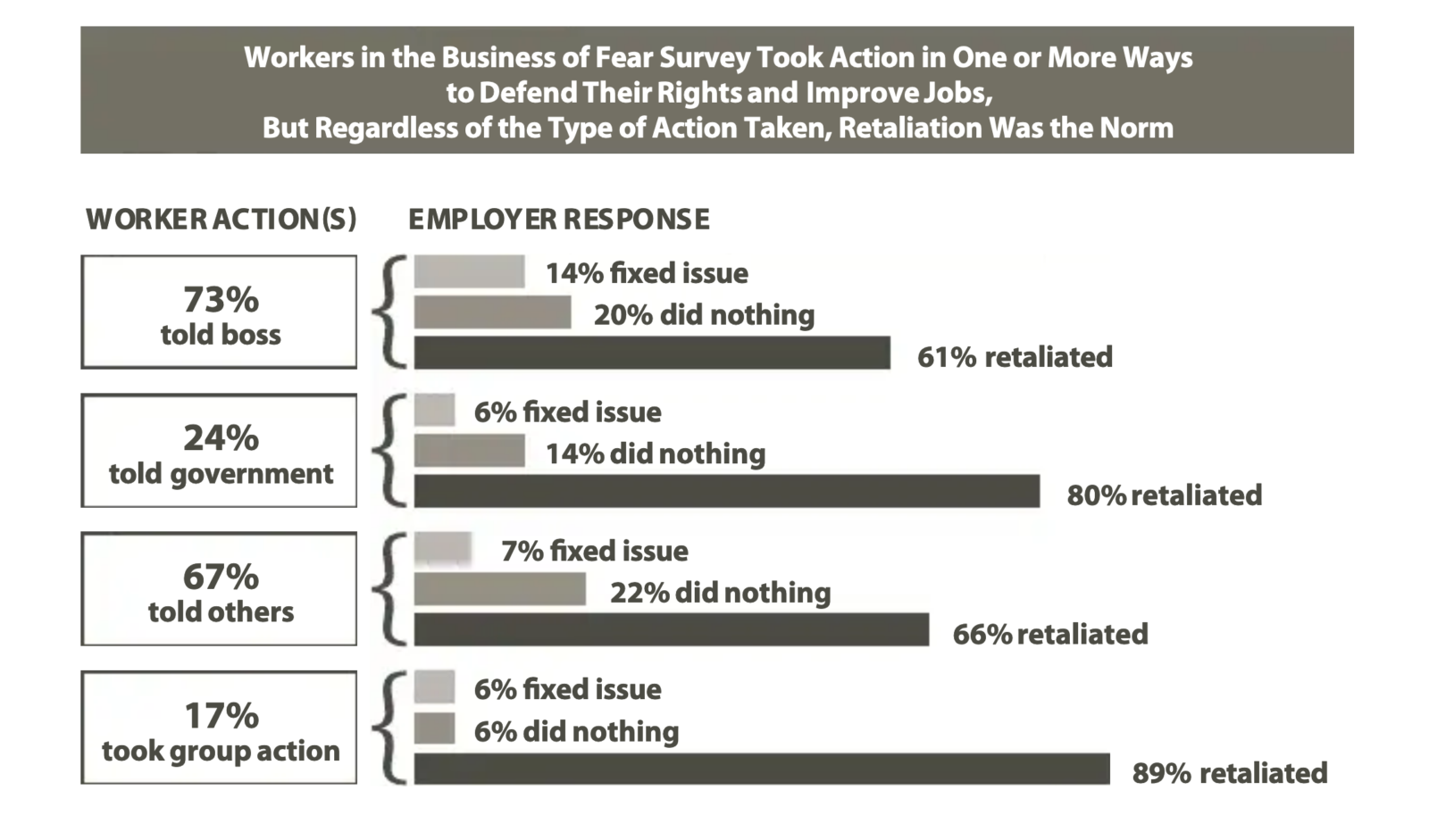

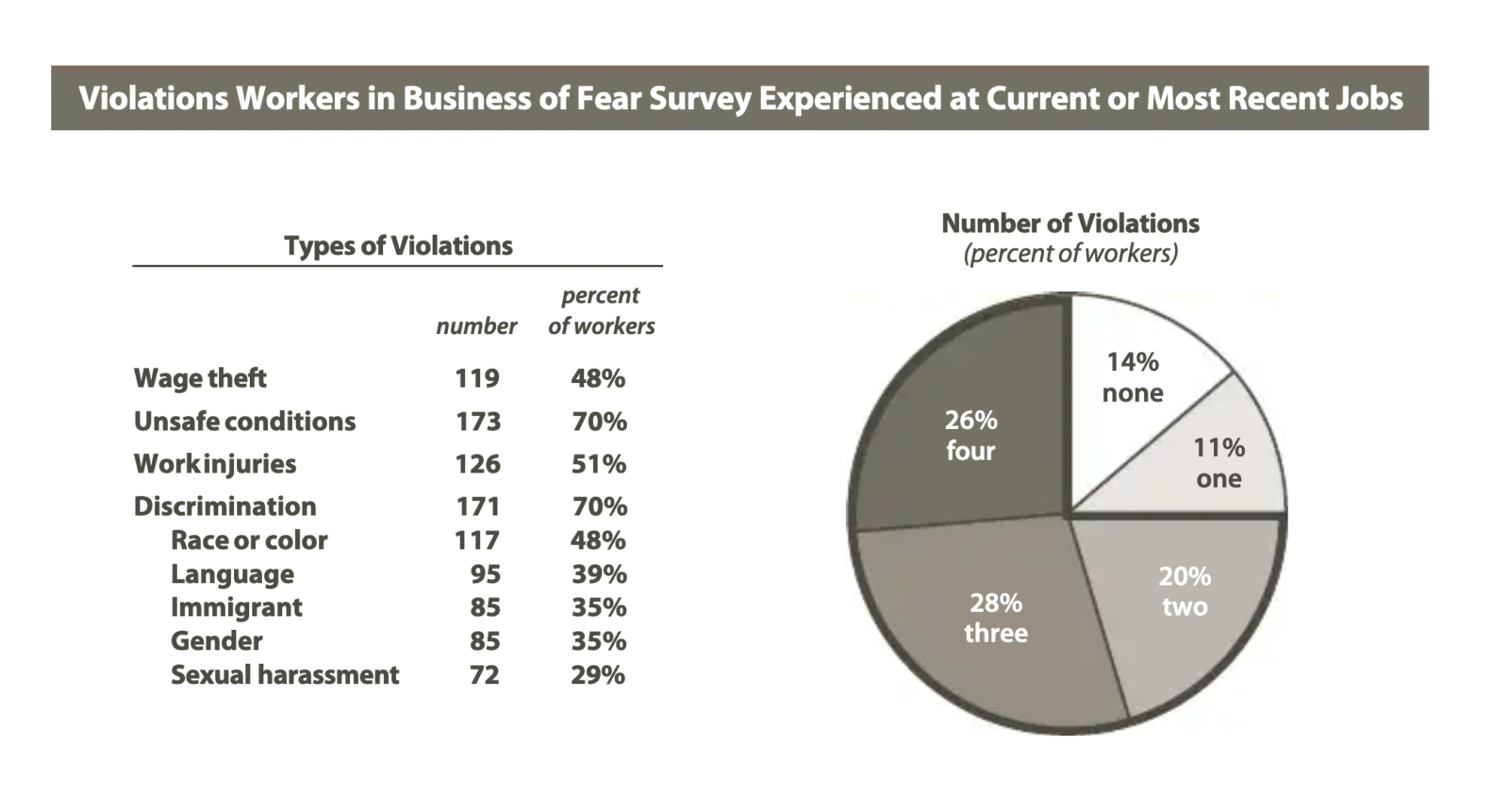

REPORT RELEASE: Challenging the Business of Fear

News

News

Baltimore Mayor Backs Public Funds for Community Land Trusts to Fight Displacement

News

News

Released from Jail, Dairy Worker Leaders Take Action at Ben & Jerry’s Harvard Square, Next up, Scoop Shops everywhere on Tuesday, April 4!

News

News

Beyond Washington Politicking, the Real Health Care Story Is in the States

News

News

Radio Dispatch interview with Ben Palmquist and Nijmie Dzurinko on the failire of the AHCA and grassroots Healthcare Is a Human Right organizing

News

News

Jamie Longazel: Barletta takes coal baron approach on health care

News

News

Ellen Schwartz on the arrest of human rights defenders José Enrique Balcazar Sanchez and Zully Victoria Palacios Rodriguez

News

News

Human Rights Leaders from Migrant Justice Targeted in Vermont

News

What the CBO revealed about the American Health Care Act

News

News

OpEd: UVMMC’S Path to a Health Care Monopoly

News

News

Professor Darrick Hamilton’s 10-Point Plan for a New Social Contract

News

News

Why We Need an Alternative Vision, Not Alternative Facts

News

News

The Growing Grassroots: A conversation with Cait Vaughan

News

News

Tomato Pickers Win Higher Pay. Can Other Workers Use Their Strategy?

News

News

Five Key Things to Know about the Republican Health Care Plan

News

News

Empleados Temporales Exigen Mejores Beneficios

News

News

¿Son justas las condiciones laborales de los trabajadores temporales?

News

News

Lawmaker, Advocates Denounce Illinois Temp Worker Mistreatment

News

News

Groups Claim Illinois Businesses Are Taking Advantage of Temp Workers

News

News

Movement for Black Lives Pushes for Victories City by City

News

News

New Data Shows Decrease in Arrests and Summonses in Schools; Communities Call for Further Decrease in School Policing

News

News

Youth and Parents will Continue the Fight for Quality Public Education for All Students

News

News

We Don’t Need a “Temporary Economy.” We Need a Responsible Job Creation Act Now

News

News

Students and Parents Across the Country Continue to Oppose Betsy DeVos’ Nomination for Secretary of Education

News

News

The latest on the attacks on health care

News

News

Women’s Rights Are Human Rights

News

News

MLK Reminds Us We Need a New Social Contract

News

News

HCHR Collaborative statement on healthcare organizing in the Trump era

News

News

Healthcare Is a Human Right campaign news

News

News

Congress deregulates drug and medical device approval, Tom Price tapped to head HHS

News

News

Human Rights Day Reminds Us to Build Opposition and Democracy for a Just Future

News

News

On Building Opposition, Not Just Resistance, to the Trump Coalition

News

News

Facing Trumpism: An Overview of Threats

News

News

Supporting Human Rights and Inclusive Democracy

News

News

What to Expect from the Coming Republican Attacks on Health Care

News

News

On Protecting Democracy & Human Rights in the Trump Era

News

News

Thank you for protecting human rights in the Trump Era

News

News

NESRI & PPF-PA publish report on healthcare in Pennsylvania

blog

blog

Workers’ Comp Hub Newsletter: Fall 2016

News

News

Op-Ed: “It’s time for insurance companies to stop putting profits ahead of people”

News

News

National Coalition Dignity in Schools Campaign Calls for Removal of Police from Schools

News

News

Arrests & Summons in NYC Schools Decrease but Deep Racial Disparities Still Remain a Concern

News

News

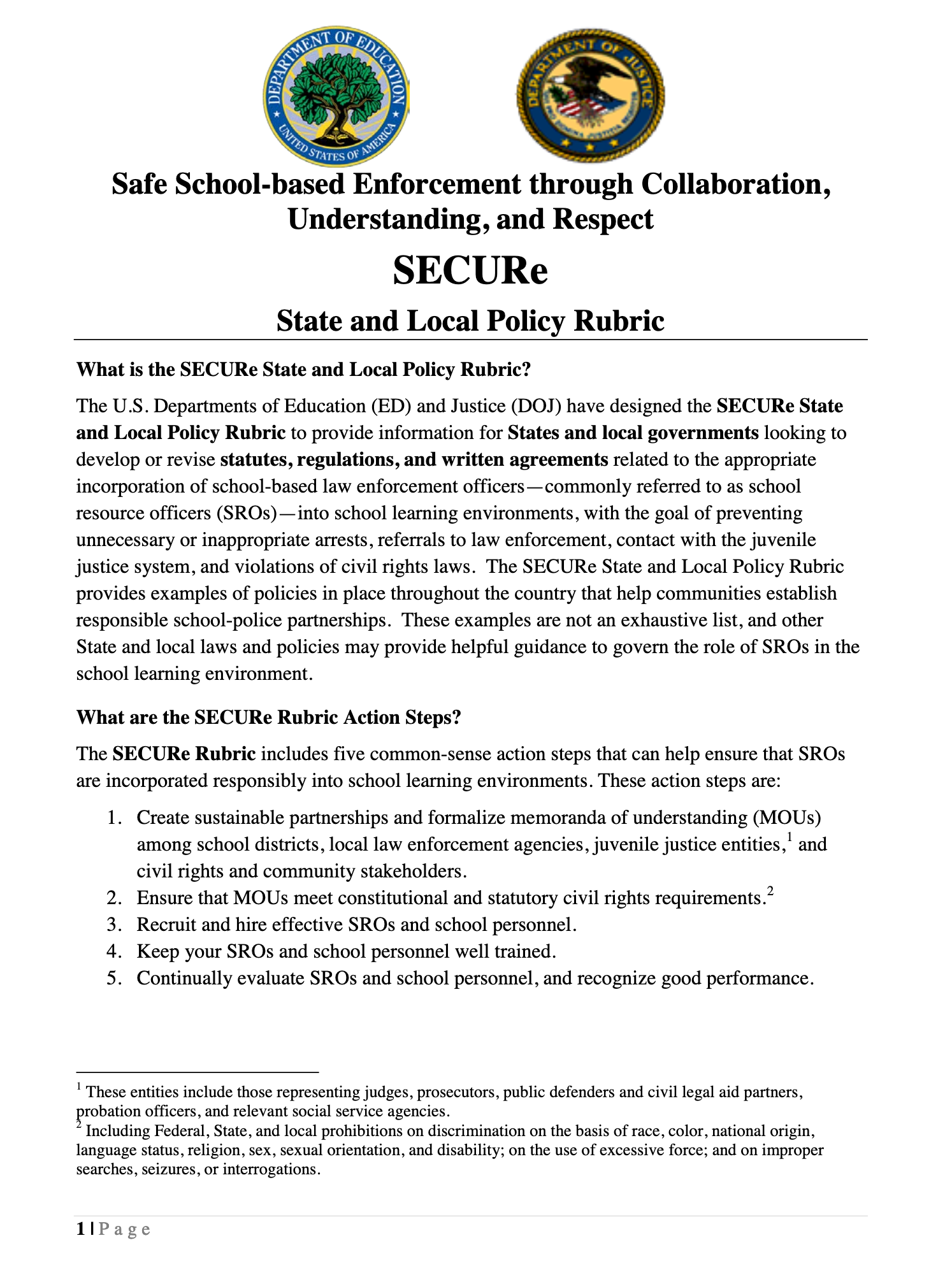

Federal Govt. Releases Guidance on Police in Schools, But Solutions Should Go Further to Call for More Counselors Not Police

News

News

Aetna and Mylan are model companies in a healthcare system that values corporate profits over human lives

News

News

Economic Justice a Core Demand in A Vision for Black Lives Policy Agenda

News

Students, Parents and Teachers Urge the City to Adopt Further Changes to Finally End the School-to-Prison Pipeline

blog

blog

Workers’ Comp Hub Newsletter: Spring/Summer 2016

News

The latest from the Healthcare Is a Human Right Collaborative

News

News

Analysis of national healthcare news

News

News

NESRI Statement on the Killings of Philando Castile, Alton Sterling and Dallas Police Officers

News

News

U.S. Secretary of Education Calls on Charter Schools to Rethink Discipline

News

News

Reflections on the Mass Shooting in Orlando

News

News

NESRI Supports Crispin Hernandez and the Right of New York Farmworkers to Organize

News

News

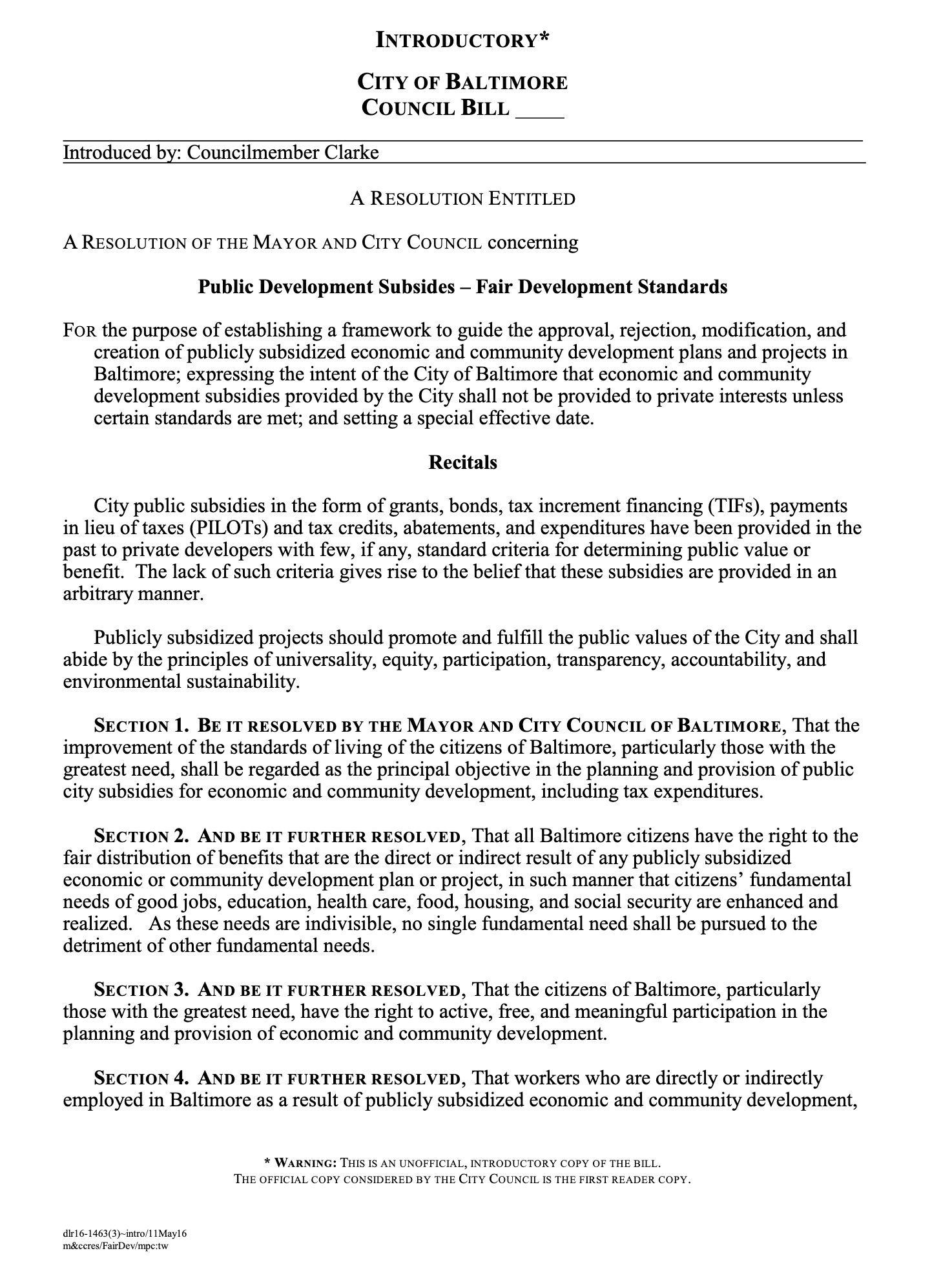

Baltimore City Council to Consider Fair Development Standards in Public Development Subsidies

News

News

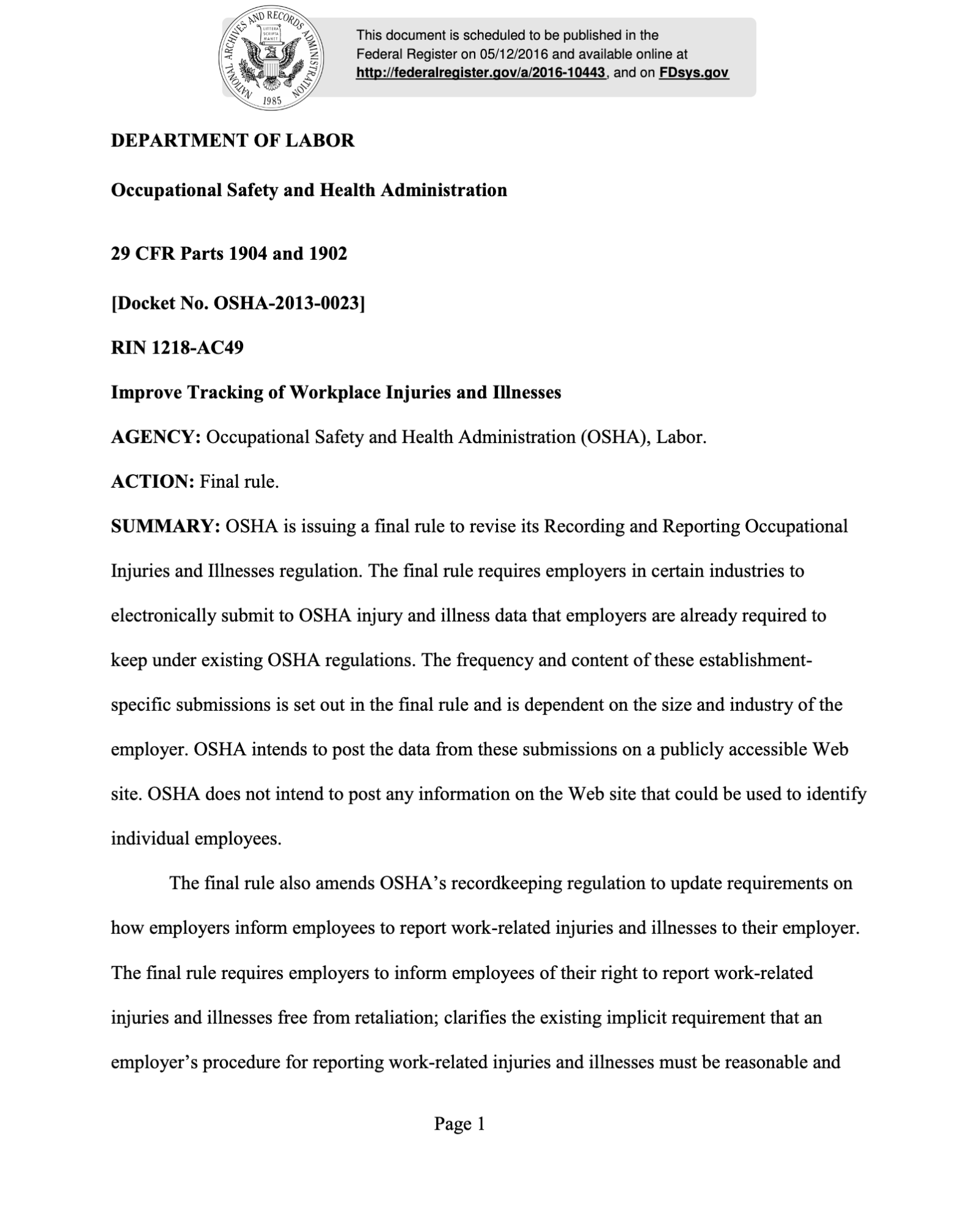

New OSHA rule to help protect workers from retaliation

News

News

Honoring Michael Ratner

News

News

DSC Members Convene in Los Angeles to Strategize to End School Pushout

News

News

Farmworkers & Consumers Declare a National Boycott of Wendy’s

blog

blog

Workers’ Comp Hub Newsletter: Winter 2016

News

News

PRESS RELEASE: Economists decry political attacks, urge serious exploration of universal, publicly financed health care

News

News

Economists call out politically motivated attacks to prevent serious exploration of universal health care

News

News